[24 April 2026]

“I’m just really angry. I didn’t sacrifice all those years when the kids were little, to not be independent today.”

Those are the heartfelt words of one of Pinnacle’s clients, Jane, in her mid 50’s.

Jane began her career in marketing straight from college, working full-time through her twenties. Like many of her generation, she entered the workforce long before automatic enrolment was introduced in 2012. Pension saving was not embedded into early working life. When she married and had children, her career shifted. She moved into consultancy and self-employment, structuring her work around family life. Her income remained healthy, but she no longer had the structure of an employer behind her.

Workplace benefit packages are not transferable. The pension itself is. But the employer contributions are not. Nor are the prompts, nudges and built-in reviews that keep long-term planning on track. When she began to work for herself, she was exposed, and she didn’t know it.

As a self-employed consultant, Jane no longer had her employer contributing alongside her, no automatic enrolment reminding her to save, no income protection and no framework ensuring regular reviews.

Like many people working for themselves, she focused on keeping income steady and clients happy. A failed marriage, young children and a new relationship added to the day-to-day demands. Even so, she felt she was succeeding at keeping on top of all the demands on her time and finances. Working for herself gave her flexibility as a single parent. But it also meant she lost the financial protection that employment provides.

Jane reflects:

“When I was growing up it was all about getting on the property ladder and that’s where you build wealth. Save little and often, buy bricks and mortar. That was the message. No one in my world was talking about investing as such outside of buying a property.

Now I think about it, I was really exposed. When I went freelance, my accountant helped me set up the business. But he didn’t talk to me about protection or long-term planning. And he didn’t suggest I needed a Financial Adviser. Looking back, I cast myself adrift.”

By the time Jane felt settled enough to revisit her finances, more than 15 years had passed since she first started work. At 44, through her new partner, she was introduced to Pinnacle. She set up a St. James’s Place pension and began contributing consistently for the first time.

Today, at 56, her position is broadly secure. Around £200,000 in pensions. A mortgage-free property worth approximately £600,000 from her first marriage. Around £100,000 in savings. On paper, she is not in difficulty. But compared to her peers, it tells a different story.

Her now second husband, Simon, followed a more traditional employed career. Continuous pension contributions. Employer support. Critical Illness cover. No extended breaks. No juggling self-employment around young children. The gap between them is not even about effort, ability or earnings. It is about lack of advice and structure early on. Jane is candid:

“I didn’t know what I didn’t know. I wasn’t consciously doing anything wrong. I just didn’t understand financial strategies like compounding or what missing those early years would mean. There were no forecasting examples, no one showing me the long-term picture and the gap I was building. No financial mentor. I’m angry, and mostly with myself.”

Why self-employment carries greater long-term risk

Being self-employed brings autonomy, flexibility and on paper often higher earnings. But it also removes the safety nets.

Employment delivers:

- Employer pension contributions

- Automatic enrolment

- Continuity during busy life stages

- Structured protection through benefit schemes

Self-employment requires every decision to be made consciously. Whether to contribute. How much. For how long. When life is busy and you’re young, it’s hard to think 30 years into the future. The long-term impact of not saving into a pension early can be significant.

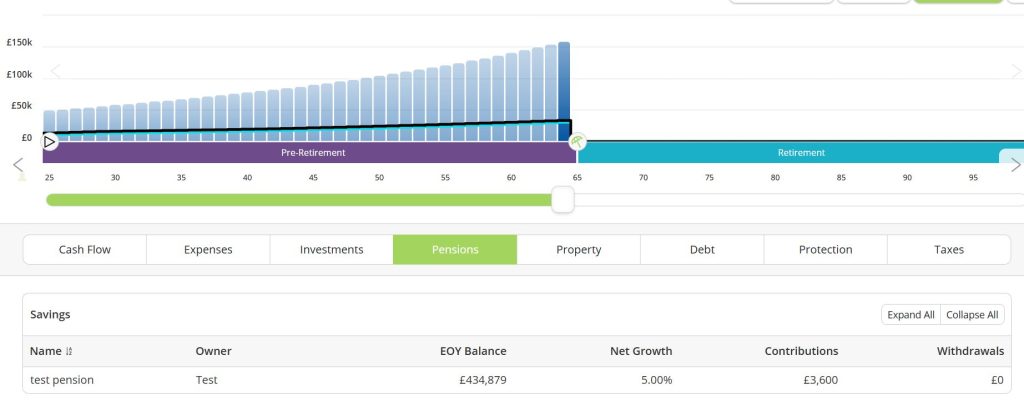

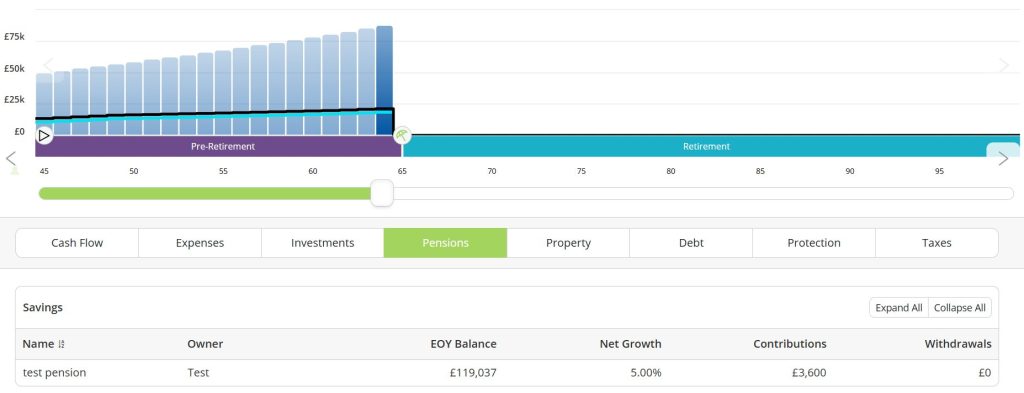

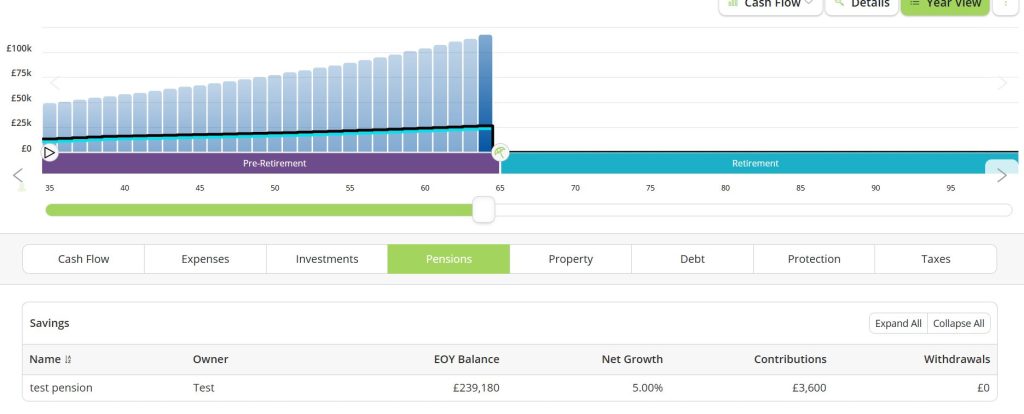

The cost of delay

Pension outcomes are driven as much by when you start as by how much you contribute.

Starting at 25 with £300 per month for 40 years could produce a pension of around £434,879.

Starting at 35 with the same contribution for 30 years might result in around £239,180.

Starting at 45 with the same contribution for 20 years could produce around £119,037.

They are not minimum and maximum amounts. What you get back depends on how your investment grows and the tax treatment of the investment. You could get back more or less than this.

Even doubling contributions later may not fully recover the lost growth. Compounding needs time. Once those early years are gone, they cannot be recreated.

This is a clear illustration of the cost of delay. And it can disproportionately affect the self-employed and those who take career breaks.

A wider issue, particularly for women

Jane’s experience reflects a broader pattern. Women are more likely to take career breaks after having children, move into consultancy or flexible work, miss employer pension contributions, and restart saving later. The result is a persistent gender pension gap as retirement approaches.

Although Jane is no longer looking at a significant financial problem during her retirement, women do make up the majority of pensioners and pensioners living in poverty. The Department for Work and Pension’s own data shows 57% of pensioners in poverty are women*. Women also live statistically longer than men and are more likely to be single in later life due to widowhood or divorce — factors that impact retirement income needs.

Jane however does feel more reliant on her second husband Simon’s pension than she would like. Her adviser explains that while the couple’s overall retirement position is strong, rebuilding Jane’s personal sense of independence is harder. And, who knows what’s around the corner? Jane now speaks openly to her friends who have their own children in their 20’s and 30’s juggling young families.

“I tell them to get proper advice as soon as they start out. I don’t want them waking up at 56 like me, angry and dependent on someone else. I worked hard. I sacrificed a lot to keep my career going while raising children. I deserve to feel confident on my own now.”

Flexible working and self-employment offer you the lifestyle you need at the time, but they require deliberate planning to give you the financial freedom in the future.

The value of an investment with St. James’s Place will be directly linked to the performance of the funds you select and the value can therefore go down as well as up. You may get back less than you invested.

The advice given to Jane was provided after a full evaluation of their specific needs, circumstances and requirements. The solutions provided may not be suitable for everyone and the information provided here does not constitute advice.

Although this case study relates to a real-life example, where we have helped our clients by providing solutions to their financial problems, the names and figures have been changed for confidentiality purposes.

*Women’s Budget Group, Women and Pensions in the UK, 28th January 2026. (wbg.org.uk)

SJP Approved 24/04/2026